20-year mortgage refinance rates fall, giving buyers savings opportunity | March 16, 2022

Our goal here at Credible Operations, Inc., NMLS Number 1681276, referred to as "Credible" below, is to give you the tools and confidence you need to improve your finances. Although we do promote products from our partner lenders, all opinions are our own.

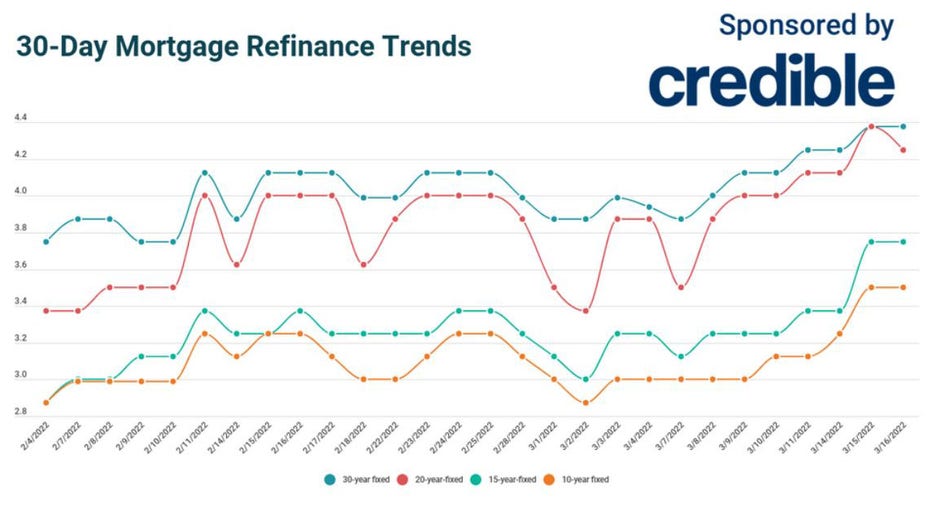

Based on data compiled by Credible, mortgage refinance rates are largely unchanged since yesterday, except for 20-year loans, which went down.

- 30-year fixed-rate refinance: 4.375%, unchanged

- 20-year fixed-rate refinance: 4.250%, down from 4.375%, -0.125

- 15-year fixed-rate refinance: 3.750%, unchanged

- 10-year fixed-rate refinance: 3.500%, unchanged

Rates last updated on March 16, 2022. These rates are based on the assumptions shown here. Actual rates may vary.

If you’re thinking of doing a cash-out refinance or refinancing your home mortgage to lower your interest rate, consider using Credible. Credible's free online tool will let you compare rates from multiple mortgage lenders. You can see prequalified rates in as little as three minutes.

What this means: Mortgage refinance interest rates rested across three key terms after yesterday’s surge, with one key rate decreasing. With 30- and 20-year rates sitting above 4% for six days in a row, shorter-term rates will offer homeowners the best opportunity for savings. Homeowners who can manage higher monthly payments may want to consider refinancing to a shorter term to take advantage of interest savings ahead of future increases.

WHAT IS CASH-OUT REFINANCING AND HOW DOES IT WORK?

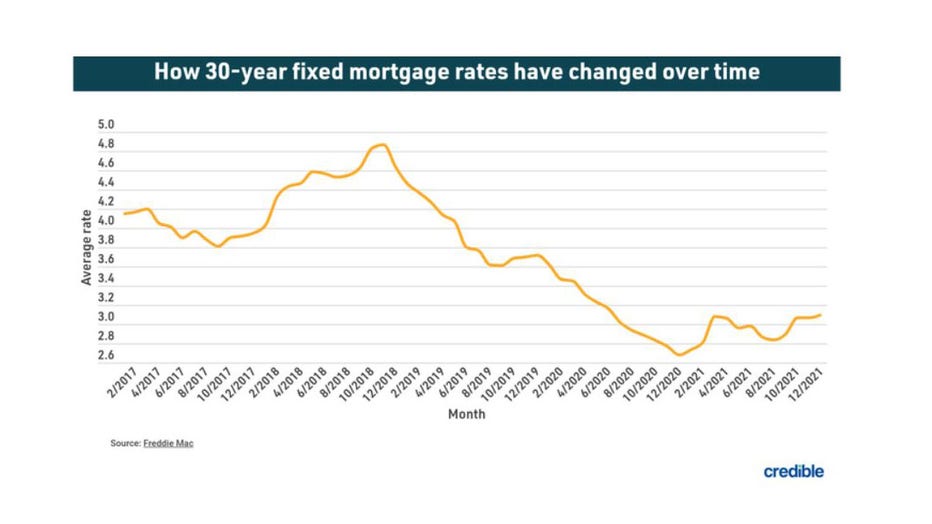

How mortgage rates have changed over time

Today’s mortgage interest rates are well below the highest annual average rate recorded by Freddie Mac — 16.63% in 1981. A year before the COVID-19 pandemic upended economies across the world, the average interest rate for a 30-year fixed-rate mortgage for 2019 was 3.94%. The average rate for 2021 was 2.96%, the lowest annual average in 30 years.

The historic drop in interest rates means homeowners who have mortgages from 2019 and older could potentially realize significant interest savings by refinancing with one of today’s lower interest rates.

If you’re ready to take advantage of current mortgage refinance rates that are below average historical lows, you can use Credible to check rates from multiple lenders.

How to get your lowest mortgage refinance rate

If you’re interested in refinancing your mortgage, improving your credit score and paying down any other debt could secure you a lower rate. It’s also a good idea to compare rates from different lenders if you're hoping to refinance so you can find the best rate for your situation.

Borrowers can save $1,500 on average over the life of their loan by shopping for just one additional rate quote, and an average of $3,000 by comparing five rate quotes, according to research from Freddie Mac.

Be sure to shop around and compare current mortgage rates from multiple mortgage lenders if you decide to refinance your mortgage. You can do this easily with Credible’s free online tool and see your prequalified rates in only three minutes.

How does Credible calculate refinance rates?

Changing economic conditions, central bank policy decisions, investor sentiment and other factors influence the movement of mortgage refinance rates. Credible average mortgage refinance rates reported in this article are calculated based on information provided by partner lenders who pay compensation to Credible.

The rates assume a borrower has a 740 credit score and is borrowing a conventional loan for a single-family home that will be their primary residence. The rates also assume no (or very low) discount points and a down payment of 20%.

Credible mortgage refinance rates reported here will only give you an idea of current average rates. The rate you receive can vary based on a number of factors.

Think it might be the right time to refinance? Be sure to shop around and compare rates with multiple mortgage lenders. You can do this easily with Credible and see your prequalified rates in only three minutes.

When is it worth it to refinance?

Refinancing a mortgage can be a great way to save money. But it’s not always the best move for every homeowner.

People refinance for a number of reasons, including to get a lower interest rate, change their monthly payment amount and lower their interest costs. Generally, if you can lower your interest rate by at least 0.75%, refinancing might be a good move.

But before you refinance, be sure to weigh closing costs, and calculate how long it will take before your savings from the refinance cover the expenses of refinancing.

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.

As a Credible authority on mortgages and personal finance, Chris Jennings has covered topics that include mortgage loans, mortgage refinancing, and more. He’s been an editor and editorial assistant in the online personal finance space for four years. His work has been featured by MSN, AOL, Yahoo Finance, and more.